Umbrella insurance protects against devastating financial loss, should you be found at fault for a car, boat, or home accident. Think of it as asset protection. Umbrella coverage is extra liability insurance, which prevents having to dip into your savings, investments, retirement fund – even future earnings – if you are sued and must pay a legal judgment, medical expenses, and/or lost wages.

In other words, umbrella coverage is a low-cost method of adding significantly more liability insurance to an existing home, auto, or boat insurance policy. It provides peace of mind, knowing you won’t go broke if someone sues – which is why umbrella liability coverage for Florida homeowners is one of the smartest forms of protection available.

Umbrella insurance may also be referred to as excess liability coverage or a personal umbrella policy (PUP).

What This Liability Coverage Includes

One of the important aspects of umbrella liability coverage for Florida homeowners is it only kicks in once the liability limit of your home, auto, or boat insurance policy is exhausted. It covers you and members of your household who don’t have insurance themselves, such as dependent children – and it covers you no matter where in the world you may travel.

The most critical protection umbrella insurance offers is liability coverage for when you are sued and found responsible for accidental injury to others or damage to their belongings/property. This includes payment of your legal expenses.

Umbrella coverage may also protect against additional types of liability claims not covered by your underlying home/auto/boat policy, such as:

- Wrongful eviction/entry

- Invasion of privacy

- Libel, slander, defamation of character

- Mental anguish

- Malicious prosecution

In short, umbrella liability coverage for Florida homeowners bridges the gap between your standard policy and a potential lawsuit. Check with the insurance professionals at The Windward Insurance Agency to find out what your umbrella coverage options are.

What Umbrella Insurance Excludes

There are a number of exclusions in the average umbrella insurance policy. For example, the following are not covered by umbrella insurance:

- Policyholder injuries or medical expenses.

- Damage to policyholder’s home, car, boat, or personal belongings.

- Intentional or criminal acts by policyholder.

- Liabilities incurred during work or professional activities. This might even include babysitting if you’re getting paid for it.

Who Needs Umbrella Liability Coverage & Why?

The question isn’t just who needs it – it’s who can afford not to have it. Umbrella liability coverage for Florida homeowners offers peace of mind for anyone with assets, property, or responsibilities worth protecting.

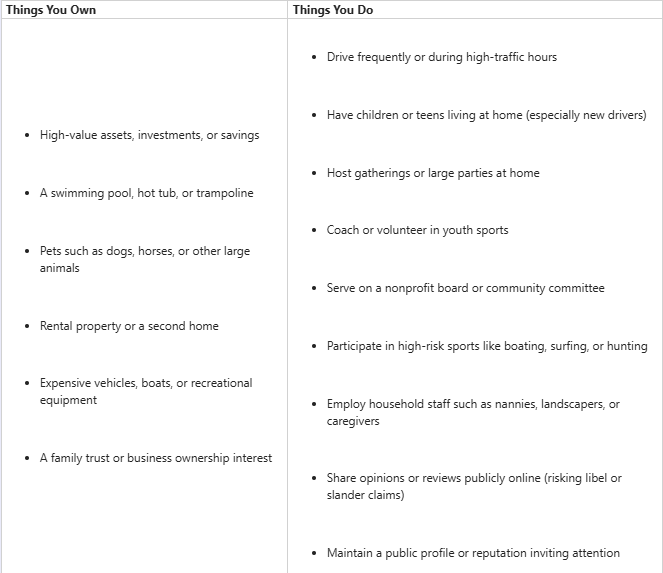

In today’s litigious world, lawsuits can happen to almost anyone. Your level of exposure often depends on what you own and what you do. The table below highlights the common factors increasing your risk of being sued:

Real-Life Examples of Umbrella Insurance in Action

Even careful homeowners can find themselves facing lawsuits after everyday accidents. Whether the claim ends in a settlement or a court judgment, if you’re found liable, you’re responsible for paying the costs. With umbrella liability coverage for Florida homeowners, those costs don’t have to come out of your savings or future earnings.

At Home

A simple mishap can escalate quickly:

- A guest slips at your holiday party and suffers a concussion.

- Your dog breaks free from the yard and injures a passerby.

- Your teenager hosts friends while you’re away, and an argument turns into injuries and property damage.

On the Road or Water

Accidents don’t stop at your front door:

- You cause a multicar crash, and your auto limits can’t cover all the vehicles involved.

- You rent a boat on vacation and accidentally damage it.

Everyday Family Life

Even seemingly harmless moments can carry liability risk:

- During a weekend baseball game, your child’s line drive breaks another player’s nose.

These real-world situations highlight how umbrella liability coverage for Florida homeowners steps in once the limits on your home, auto, or boat insurance are exhausted.

For instance, if a court awards $1 million in damages, this is roughly $700,000 more than most standard policies cover. Instead of paying this balance yourself, your umbrella policy would take care of it – after your deductible – helping to protect both your current assets and your financial future.

Umbrella Liability Coverage: Surprisingly Affordable Protection

Umbrella coverage is remarkably affordable, especially compared with other types of insurance. After all, it requires you to have an underlying home, auto, or boat policy with certain minimum liability coverage limits.

Umbrella insurance may range between $300 - $600 for $1 million in coverage, with each additional $1 million in coverage costing significantly less. You’ll want to be sure to get enough to cover your net worth, which is what you might lose in a lawsuit. You should also consider your potential future income, such as if you are expecting to inherit a large sum or are currently a medical student expecting to make much more in the future.

Bundling – buying your umbrella coverage with the same insurer providing your home/auto/boat policy – can often save you money. In addition, where you live, your credit history, driving record, and insurance claims history can all impact how much you pay. And, of course, the more assets you have, the higher the cost of umbrella insurance.

Considering the protection it provides, umbrella liability coverage for Florida homeowners is one of the most cost-effective ways to safeguard wealth.

Bundle & Save: Add Umbrella Liability Protection to Your Policy

If you’re looking for umbrella liability coverage for Florida homeowners to complement your existing home, auto, or boat insurance policy, contact the insurance professionals at The Windward Insurance Agency. We can provide you the best available options.

Get a quote for umbrella insurance on our website or call us at (866) 231-2433 for personalized assistance. You can also visit our umbrella insurance webpage for additional details.

.png)